https://www.api.org/news-policy-and-issues/blog/2019/06/12/growing-us-energy-revolution-keeps-exceeding-expectations

The U.S. energy revolution continues to surge ahead – but you might not know it from some recent headlines:

“The Shale Boom Is About To Go Bust” (Oil Price.com)

“Oil Wells Aren’t Producing as Much as Forecast” (Wall Street Journal)

“U.S. Oil Production Is Headed For A Quick Decline” (Oil Price.com)

Actually, domestic natural gas and oil production continues to expand. See API’s most recent Monthly Statistical Report. For some of the same reasons economists are so bad at predicting recessions, sometimes analysts may struggle to accurately project where U.S. energy is heading. After all, the shale revolution’s prospects have been underestimated since it launched.

Look at the facts. There have been strong and demonstrable productivity gains. Another indicator is that after the first few years of a shale well’s life, production had generally tended to decline more slowly than conventional production. This means that relatively small but steady long-term production has continued from shale drill wells, which is something that was expected but unproven a decade ago when shale production was nascent.

With the benefit of experience, and as shale production has come to represent the majority of U.S. oil and natural gas production, the United States’ total drop-off in existing oil and natural gas production has slowed over the past few years and consequently contributed to U.S. production exceeding expectations. In turn, this has implications for U.S. energy policy as well as the oil and natural gas industry, its infrastructure and the markets that it needs.

Let’s shed light on some key developments.

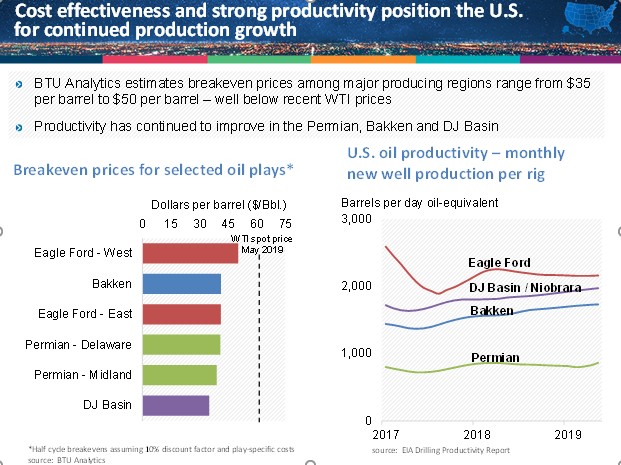

First, what oil price is needed for a company to break even on drilling a well? According to BTU Analytics, this figure as of May 2019 ranged from $35 per barrel to $41 per barrel for all but one of the major oil shale-producing regions in the U.S. Only the western area of the Eagle Ford region in South Texas was higher at about $50 per barrel – and even that was below recent West Texas Intermediate crude oil prices of about $60 per barrel. This means that drilling for oil should be profitable across every major U.S. producing region.

These estimated breakeven prices have remained relatively low because the productivity of wells has generally improved. In its monthly Drilling Productivity Report, the U.S. Energy Information Administration (EIA) reports that productivity has broadly risen in the Permian Basin (West Texas, New Mexico), Bakken formation (North Dakota, Montana), and Denver-Julesburg (DJ) Basin / Niobrara (Colorado, Wyoming). Even the Eagle Ford’s overall productivity has exceeded what it was in mid-2017.

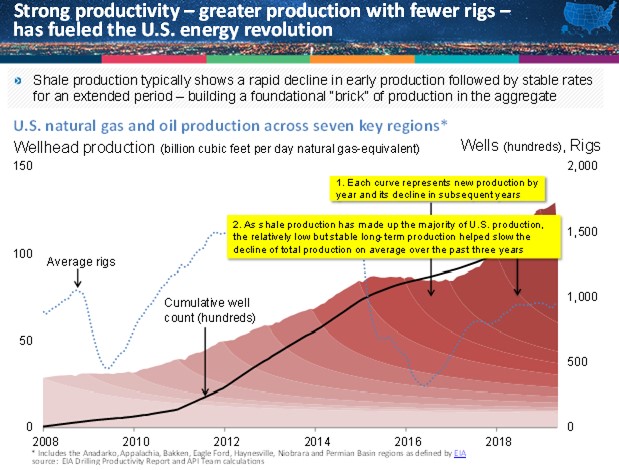

Next, with snapshots of these individual areas, what’s the big picture look like? A nationwide view of total shale oil and natural gas production follows, based on the EIA’s detailed data by producing region.

Total production, as shown, increased steadily from 2010 to 2014 and then hit a setback in drilling activity as global oil prices fell by half or more from over $100 per barrel through much of 2014. As the industry became more efficient and innovated to thrive in a low-price environment, total production resumed climbing in the fourth quarter of 2016 and has risen since then at an even faster rate than it did before the downturn.

Thanks to productivity gains, this increased production has been achieved with more than one-third fewer drill rigs than in 2014. At the same time, it has required relatively fewer wells to achieve record production, as wells now tend to be longer and targeted better than they were in the past.

While these developments are impressive, there’s a critical story buried in the details

The picture in the second graph above shows the new production that comes on stream each year, depicted as individual shaded areas from 2008 through the first quarter of 2019. Production naturally declines over time, and shale well production initially declines faster than conventional production.

However, something remarkable has happened since 2017: The rate of decline in overall U.S. shale production decreased to a three-year average of about 14 percent and in 2018 hit its lowest level (12.5 percent) since before the energy revolution, based on EIA’s Drilling Productivity Report and API’s team calculations.

How so? New techniques to re-vitalize existing wells are part of it. More importantly, as Jim Jarrell of RS Energy Group predicted in 2010, the historical data tell us that, after the steep initial decline shale production, shale production over the longer duration of a well’s life tends to decline at a relatively slower rate compared with that of conventional production. Consequently, as shale production has come to make up the majority of total U.S. production, annual U.S. shale production in the aggregate has tended to steady like a foundational “brick.”

Ultimately, this means the U.S. energy revolution is likely to continue to exceed expectations for a long time, provided we collectively plan forward to enable the energy revolution by fostering technical and process innovations; enabling infrastructure to expand for pipelines, processing, and exports; and, maintaining trusted trade relationships, especially across North America.

If we do these things, we should enjoy tangible benefits and great news for our nation’s economy and energy security for decades to come.